China will start selling the first batch of its 1 trillion yuan ($138 billion) of ultra-long special sovereign bonds on Friday, as officials ramp up efforts to support the world’s No. 2 economy.

The central government will begin by issuing 30-year bonds, according to a notice by the Ministry of Finance. That ended months of speculation over when the bonds — only the fourth of their kind in 26 years — would be rolled out, after the ruling Communist Party announced its plan for them in March.

Bonds with 20-year and 50-year tenors will be offered from May 24 and June 14, respectively. Auctions of the securities will continue until a final batch consisting of 30-year notes goes on sale in November. The ministry didn’t disclose the amount of bonds to be sold.

The bond sales are expected to bolster this year’s growth by 1 percentage point, according to Xing Zhaopeng at Australia & New Zealand Banking Group.

“The timing of the bond issuance is likely intended at offsetting the impact” of protectionist tariffs the US is threatening to take against Chinese goods, he said, also citing uncertainty ahead from a Communist Party huddle on reforms set for July.

Bloomberg reported the special sovereign bonds sale earlier on Monday. The issuance will include 300 billion yuan of 20-year bonds, 600 billion yuan of 30-year notes and 100 billion yuan in the 50-year tenor, according to people familiar with the matter, who asked not to be identified as the information is private.

Investors responded positively to the bond sales news, with the benchmark CSI 300 Index of onshore shares paring an earlier loss of 0.9%. Chinese equities in Hong Kong erased an earlier loss to rise 0.4% as of 2:35 p.m. local time.

Chinese bonds rallied on Monday as disappointing credit data fueled expectation of more monetary easing and allowed traders to shrug off concerns over a looming spike in government debt supply. The yield on 10-year government bonds fell to 2.29%.

President Xi Jinping’s government is stepping up fiscal support to help the economy, which is facing pressure from a housing crisis and dampened consumer confidence. Beijing announced plans for the bond sale during the National People’s Congress, where policymakers also unveiled an ambitious annual growth goal of about 5%, which economists say will require more stimulus.

Analysts raised expectations for the People’s Bank of China to lower the amount of money lenders must hold in reserve, to free up cash to buy bonds. Ding Shuang, chief economist for Greater China and North Asia at Standard Chartered Plc, forecast a 25-basis point reduction to the RRR to coincide with the bond sale, and saw an increased chance of a loan prime rate cut.

The bonds “increase the chance of achieving 5% growth,” he added, noting that if the government didn’t issue them soon it would be hard to deploy all the funds this year.

The planned sale comes after a broad credit measure shrank for the first time in April, amid a slew of disappointing data. Exports remain the bright spot in the economy this year, but face uncertainty as tensions between China and some of its biggest trading partners are escalating amid complaints over its excess manufacturing capacity.

Chinese authorities and policy banks slashed their bond issuance by half in the first quarter compared to last year, as local authorities loaded up with too much debt were restricted from borrowing. Funds raised from last year’s sales raised were still being deployed, diminishing the need for more action.

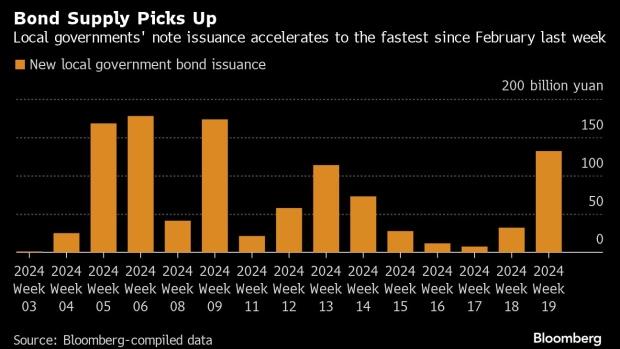

Still after that early slump, bond sales have been accelerating. Provincial governments sold the highest amount of new notes last week since February, responding to a call by top leaders to speed up local bond issuance. The 24-man Politburo also vowed in April to start the sale of special sovereign debt “at an early date.”

While the planned sales beginning this week should help make up for that slow start, they won’t compensate for still-weak loan demand from households and companies. It will also take a while for the effects of the upcoming borrowing to filter through to the real economy.

Government spending on infrastructure — which the bonds could help toward — will be key to ensuring China achieve its GDP target, which remains above economists’ forecasts, even after robust data in the first quarter. Consumer demand is still weak as a property crisis persists and the job market remains gloomy.

China will likely rely more on fiscal stimulus to support domestic demand given the continued pressure on the yuan, said Serena Zhou, senior China economist at Mizuho Securities Asia Limited.

“While we are not sure about the issuance size of the first batch of ultra-long bonds, we doubt that it will deliver a significant squeeze to the onshore rates market,” she said.

{kind=link}